The concept of banking first emerged sometime around 2,000 BC in Mesopotamia, where merchants felt the need to give out loans to farmers and traders who roamed the different cities. From then on, as trade and the economy grew, modern financial institutions were built to consolidate the scattering of economic activities and provide trust.

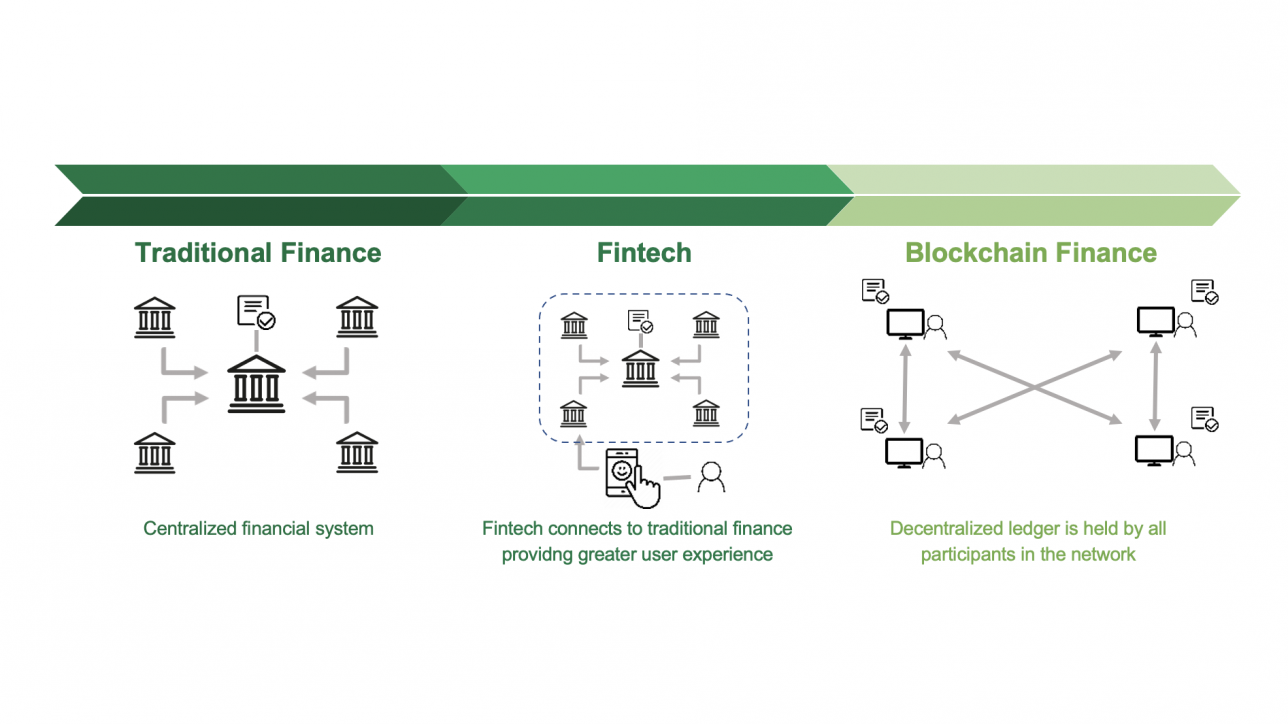

For centuries, the financial system has been heavily centralized. Along with other government entities, financial institutions joined hands to govern almost all transactions, from money issuance to lending and investing. They have this power to centralize because they alone can keep track of all financial transactions. The invention of blockchain will change the fundamental mechanics of how this new era of the financial system operates with its decentralized record-keeping feature. Once this technology fully matures, traditional financial institutions as we know them will have a lesser role in the financial system.

Blockchain and Its Promise to the Financial System

Blockchain is a decentralized record-keeping system that documents all transactions that happened on it. In other words, it is a bank book that everyone can possess and whose content is self-updating with all new transactions and the change in ownership of any assets. It defies financial institutions’ fundamental role as the centralized record keepers who prevent the same money from being spent twice or the same asset being transferred repeatedly.

Fully mature blockchain technology promises to provide greater efficiency, lower transaction costs, better transparency, a speedier rate of financial innovation, and a much lower carbon footprint (still heavily debated) compared to the traditional financial system.

The Inception of Blockchain Finance

In the early days of blockchain finance, Satoshi Nakamoto (pseudo name – actual identity remains unknown) invented Bitcoin (whose underlying technology later became known as blockchain), a digital currency to aid in the decentralized transfer of money. The transfer data stored in Bitcoin’s blockchain is static – meaning that the blockchain can only record that Entity A transfers B amount of money to Entity C.

Ethereum then came along and introduced smart contract technology, which allows blockchain to be programmable. Ethereum blockchain can instruct that only when Event D happens, Entity A can transfer B amount of money to Entity C. Any transactions can become fully automated upon a defined set of rules.

Both technologies were the foundation of the concept of what is now known as Blockchain Finance.

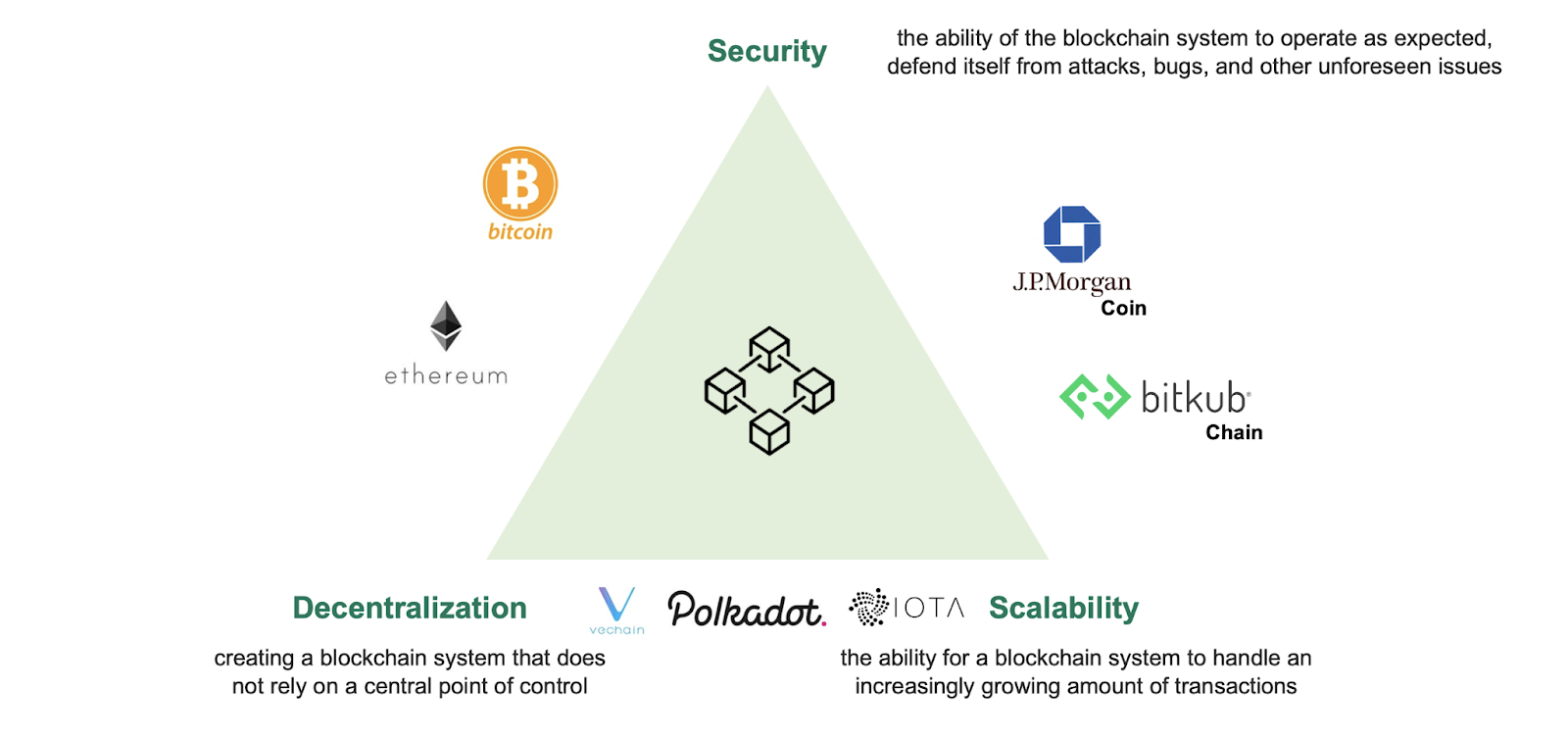

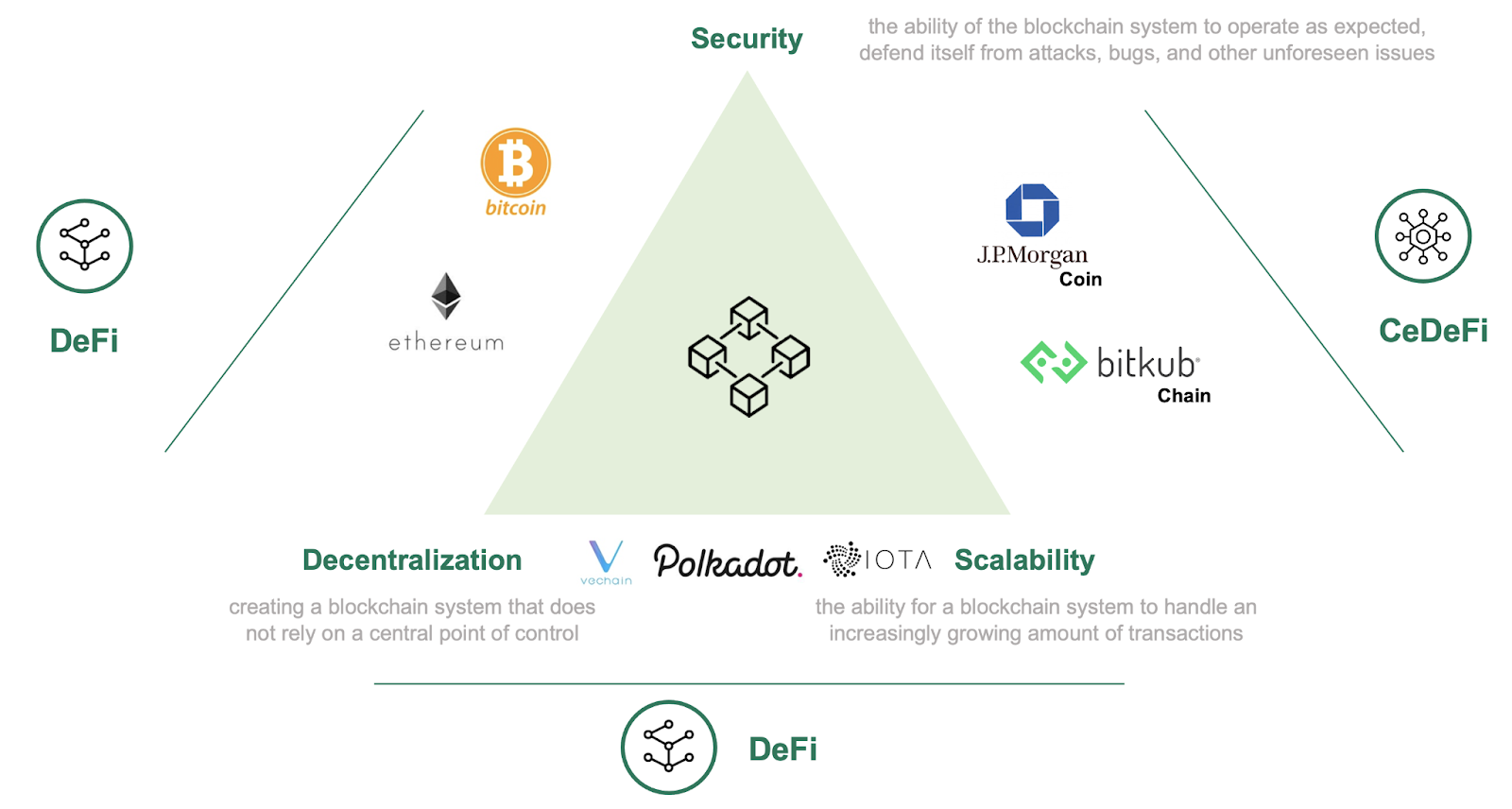

The Blockchain Finance Dilemma

While groundbreaking, current blockchain finance is not without limitations. The challenge lies in the Blockchain Dilemma – that blockchains may only choose up to two qualities to achieve: Security, Scalability, and Decentralization. The limitation is the mechanism to how each party in blockchain finance agrees that a transaction is legitimate and therefore should get updated in everybody’s copy of the bank book (referred to as the “Consensus Mechanism”).

Source: Original framework by Certik, adapted by Beacon VC

Since both Bitcoin and Ethereum prioritizes Security and Decentralization, scalability is a challenge for both blockchains. In order for a new transaction to be recorded in everyone’s copy of the bank book, someone who holds a copy of the bank book must confirm that the transaction is legitimate through the computation of a complex mathematical equation. That person is referred to as a miner, and the first miner who gets the equation right wins a monetary reward. This process of solving a mathematical equation to confirm a transaction is called the proof-of-work consensus mechanism (PoW).

Other blockchains prioritize Decentralization and Scalability, giving birth to the proof-of-stake consensus mechanism (PoS). Blockchains that adopt PoS include Polkadot and Vechain. Under the PoS concept, a miner can be eligible to confirm a transaction by putting down a ‘ stake’ in the form of coins belonging to that blockchain (think of it as a refundable deposit). The more coins put down by a specific miner, the more eligibility that miner has to validate a transaction. This consensus mechanism works because the miners who are not validating any specific transactions are obliged to check the work of the validating miners. Faulty confirmation of a transaction is penalized by confiscation of stake.

Finally, other blockchains prioritize Security and Scalability. While many blockchains use the PoS to validate transactions, we have seen a rise in the proof-of-authority consensus mechanism (PoA). In this case, new transactions are confirmed by a few authorized players in that blockchain. These players are incentivized to keep transaction data legitimate and enjoy the monetary benefit for that blockchain growth. Examples of blockchains that prioritize security and scalability include blockchain consortiums formed by financial institutions (JPM coin), and the Bitkub chain. In reality, there are many other ways that a blockchain can achieve scalability and security, as we also see cases using a hybrid model between PoS and PoA – the delegated proof-of-stake mechanism (dPOS), which we will leave for another discussion.

The Two School of Thought of Blockchain Finance (CeDeFi/ DeFi)

There are big debates in the blockchain finance space whether blockchain finance should be centralized (CeDeFi or CeFi) or decentralized (DeFi).

CeDeFi is an evolution of the current financial system where an intermediary helps manage the transaction and regulate the users’ activities in that ecosystem. Under this scenario, if a user wants to make a transaction, the user needs to create an account with the company, deposit cash or any assets into the company’s custodian, and use that company to execute the transaction. In this case, the customer would need to reveal their personal information to participate in the ecosystem. Great examples of CeDeFi platforms include Binance and Coinbase.

Conversely, with the growing need to protect own data and distrust in institutions comes the demand for DeFi. Users are required to manage their own funds and financial activities. They must have a personal wallet where they store their assets and use that wallet to carry out transactions by connecting it with decentralized service providers. Since these decentralized service providers execute trades based on smart contracts, the transactions automatically occur when conditions are met. There is zero need for human intervention. This gives flexibility for DeFi users to select service providers whose set of rules they like the most.

Which School of Thought Will Prevail?

Although there is no guarantee which school of thought will prevail, or that there will be any clear winner, we anticipate that CeDeFi will gain mass acceptance and adoption for real commercial purposes first, despite the current boom in DeFi which has been driven by speculative forces.

It is all about the evolution of public trust. CeDeFi is, by design, a bridge for general customers to start exploring the blockchain finance ecosystem and shifting their trust away from financial institutions/centralized governing entities to service providers (think of Binance, Bitkub, Zipmex, Satang Pro, etc.). These companies excel in replicating the same user experience a customer would have if they were to interact with general fintech that people know and have grown accustomed to. Once more people start adopting CeDeFi, and the infrastructure and interface for DeFi are in place, the public will soon learn to shift trust from said service providers to algorithms (code and rules of how transactions are made), leading to the potential mass adoption of DeFi. It is impossible to say when mass DeFi adoption will happen, but we can definitely see both CeDeFi and DeFi co-existing in the foreseeable future.

Such co-existence can take place in a number of manners:

- Gateway: Since value creation in the economy is still largely driven and transacted in the physical world, CeDeFi can exist as a gateway for users to convert traditional assets (such as fiat money) into decentralized blockchain finance. We are already starting to see this symbiotic relationship between CeDeFi and DeFi, in which users convert their money into digital assets using CeDeFi and then transfer it to their personal DeFi wallet. (think of Fiat -> Binance -> Metamask wallet)

- Market Segmentation: It is possible that CeDeFi and DeFi can co-exist by serving different markets in the economy. Segmentation can be based on the need for governance. For instance, CeDeFi can serve segments where visibility and governance are critical, such as corporate clients, while DeFi can serve the retail market. Segmentation can also be based on the type of trust users require. Conventional users can use CeDeFi because their trust system is based on having a single entity to point to when things go wrong, while DeFi users can be more comfortable with the algorithm.

- Business Extension: CeDeFi organizations can use DeFi as a place to experiment with financial innovations and later acquire the know-how to build or integrate similar services to their platform. This is the same model that we already see in the financial industry, in which big financial institutions leverage the capability of startups to enhance the robustness of their offerings.

While this migration unfolds, regulators and financial intermediaries incumbents will likely try to slow the migration rate to a minimum. This is because they will first need to find a satisfactory framework to thrive in an entirely DeFi environment. After all, there are certain benefits to centralization, such as the ability for the government and banks to control fund flow, regulate the market, and effectively pull monetary levers to protect the economy or national interests.

What’s Next for Financial Institutions?

There is no telling when mass CeDeFi or DeFi adoption will happen, but it is paramount that financial institutions start finding their role in this emerging ecosystem. To start from an inside-out perspective, financial institutions were built upon trust and efficiency through consolidation. The critical area of exploration is where financial institutions can continue to deliver benefits both in the CeDeFi or DeFi context. From an outside-in approach, financial institutions can navigate through different blockchain layers and access points in the ecosystem to identify a natural fit for their current products, capabilities, or future strategy and monetization models.

While we are racing towards what may be the most significant overhaul of the financial system in modern history, we must strive to remember that different populations adopt technology at different rates and that meaningful innovation must not further marginalize anyone.

Author: Woraphot Kingkawkantong (Ping)

Editor: Krongkamol Deleon (Joy)

Special shout-out: Wanwares Boonkong (Pin), Phanthila Saengthong (Mook), Panuchanad Phunkitjakran (Pook), Napat Nantavechsanti (Jum+), Phongsuphat Kanchanakom (Monn)